Most CFOs use the terms “actuarial model” and “financial model” interchangeably. Auditors don’t.

When a loyalty program’s liability estimate shows up in a 10-K footnote, the difference determines whether the number survives an audit or becomes a restatement. An actuarial model quantifies the uncertainty around redemption behavior using distributional assumptions and statistical techniques. A financial model projects outcomes using point estimates and scenario sensitivities. Both have a role. Using the wrong one for a loyalty liability is why audit files get flagged.

This piece walks through the distinction in plain English — starting with what actuarial modeling actually is — and explains when each approach is appropriate for loyalty program finance leaders.

What Is Actuarial Modeling?

Actuarial modeling is a quantitative method used to estimate the probability and financial impact of future uncertain events. Where financial models project a single outcome based on assumed inputs, actuarial models treat uncertainty itself as something to be measured using statistical distributions, historical data, and probabilistic techniques to produce ranges of outcomes rather than point estimates.

The profession traces its roots to insurance and pensions, where organizations have always needed to price risk that won’t materialize for years or decades. Actuaries don’t predict the future — they quantify how wrong the future might be, and by how much.

How actuaries differ from financial analysts and data scientists

All three roles use models. The distinction is in what they’re modeling and how they handle uncertainty:

- Financial analysts build models to project revenue, cost, and return. Inputs are usually assumed or benchmarked; the output is a single forecast. Uncertainty is addressed through scenario analysis (“what if redemption rates rise 5%?”).

- Data scientists build models to identify patterns and predict behavior. The focus is on predictive accuracy for individual-level decisions (who is likely to churn, what offer will convert).

- Actuaries build models to quantify the aggregate financial risk of uncertain future events. The focus is on the shape of the distribution — not just the expected value, but the variance, the tail risk, and the confidence interval that can be defended to a standard-setting body or auditor.

For a loyalty program liability sitting on a public company’s balance sheet, that last distinction is what matters. The liability isn’t just a number — it’s a number with a defensible range, backed by a credentialed professional opinion.

What actuarial modeling looks like in practice

An actuarial model for loyalty program liability typically includes:

- Cohort redemption curves: How redemption behavior develops over time for members who earned points in a given period

- Breakage estimation: The portion of points statistically expected to never be redeemed, estimated using survival analysis or similar methods

- Confidence intervals: A range (e.g., 90th percentile) around the central estimate, used to stress-test the liability

- Assumption documentation: Explicit, auditable records of every input and its actuarial basis

This is structurally different from plugging an industry-standard redemption rate into a spreadsheet — and it’s why auditors treat the two differently.

What Is Financial Modeling?

Financial modeling is the process of building a structured representation of a business’s financial performance, typically in a spreadsheet. Financial models are used to forecast revenue, project costs, evaluate investments, and build business cases. They rely on assumptions — redemption rates, churn percentages, average point values — that are often derived from benchmarks, historical averages, or management estimates.

Financial models are excellent tools for planning and decision-making. They answer questions like: “What happens to our P&L if redemption rates increase by 10%?” or “What’s the ROI of adding a new redemption partner?”

What they’re not designed to do is quantify the statistical uncertainty around those assumptions. A financial model will tell you the outcome given a redemption rate. An actuarial model will tell you whether that redemption rate is right, how confident you should be in it, and what the liability looks like across the range of plausible values.

The Key Differences Between Financial Modeling and Actuarial Modeling

| Actuarial Modeling vs. Financial Modeling | ||

| Financial Modeling | Actuarial Modeling | |

|---|---|---|

| Primary inputs | Assumed benchmarks, management estimates | Granular member-level transaction data |

| Output | Point estimate / single scenario | Distribution of outcomes with confidence intervals |

| Redemption rate | Fixed input or scenario-tested assumption | Estimated statistically from member behavior data |

| Validation method | Sensitivity & scenario analysis | Actuarial peer review, assumption testing |

| Audit posture | Requires justification of assumed inputs | Defensible under GAAP/ASC 606; credentialed opinion |

Many finance leaders assume that if they have a financial model for their loyalty program, they also have a reliable liability estimate.

In reality, financial models and actuarial models serve very different purposes—and using the wrong one for liability estimation can have serious consequences.

Let’s break down the key differences between the two.

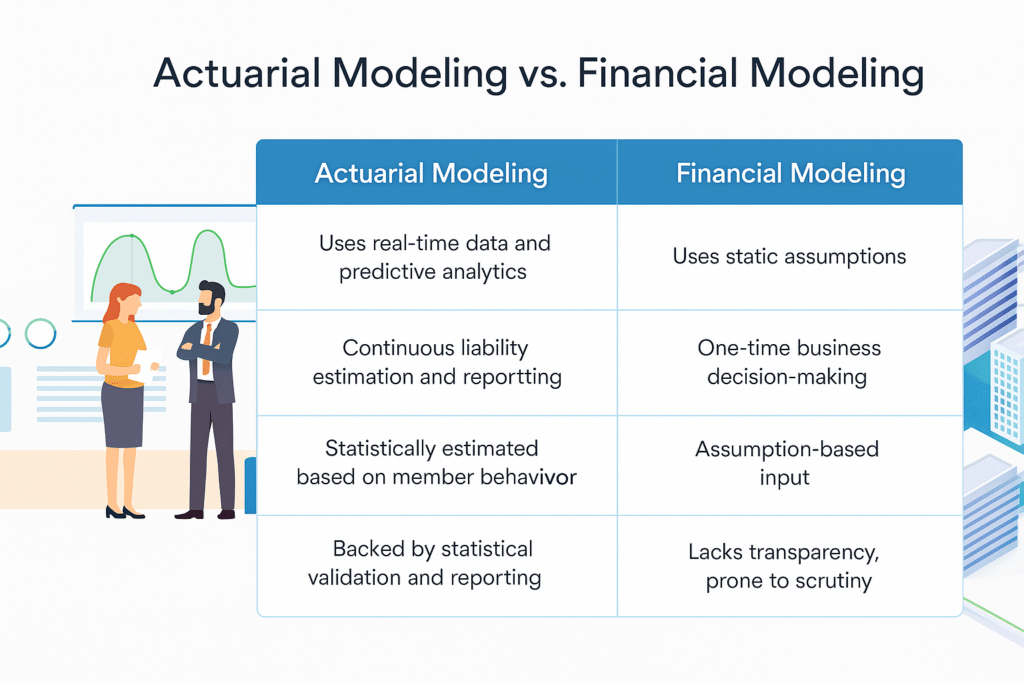

1. Assumptions vs. Data-Driven Insights

Financial models rely on high-level assumptions. They use industry benchmarks or fixed inputs, such as an assumed Ultimate Redemption Rate (URR), to estimate liability.

Actuarial models, on the other hand, are built using massive volumes of real data. Rather than assuming a redemption rate, actuarial models extract behavioral patterns from loyalty program members to directly estimate URR with statistical accuracy.

What’s the impact? A financial model might assume a 75% redemption rate, but where did this estimate come from and how is it justified?The financial model didn’t produce this estimate; it was plugged in as an assumption. An actuarial model, on the other hand, analyzes customer data at a granular level to directly estimate the URR using robust statistical and actuarial methods so the accuracy can be easily justified and documented.The actuarial model may find that the 75% assumption to be wrong, and the true URR is 90%. In this case, you’d be running your loyalty business model with a materially wrong understanding of your cost structure.Redemption cost is often the single largest expense in the business model, so this is a significant issue. If you didn’t have an actuarial model in place, you would be digging a huge financial hole in your business and wouldn’t even know it.

2. One-Time Use vs. Continuous Monitoring

Financial models are typically used once—for example, when building a business case for launching or adjusting a loyalty program.

Actuarial models are designed for continuous, real-time monitoring of liability. Since redemption behavior shifts over time, actuarial models dynamically update, ensuring ongoing accuracy in liability estimation.

What’s the impact? A financial model from five years ago may assume a redemption rate that no longer reflects current customer behavior.An actuarial model, however, continuously updates based on real-time data, accounting for recent trends such as increased engagement from a new partnership or reduced redemptions due to economic downturns.Without these updates, finance teams risk misallocating reserves, either tying up unnecessary capital or underfunding liabilities, leading to financial instability.

3. Static Estimates vs. Predictive Forecasting

Financial models generate a static estimate at a given point in time. They provide a snapshot but don’t predict how liability will shift over time.

Actuarial models leverage predictive analytics to forecast liability trends, giving finance leaders a forward-looking view that allows them to adjust business strategies proactively.

What’s the impact? A financial model might state, “Your ultimate redemption rate is 80%,” treating it as a fixed number that doesn’t change over the course of the year. However, an actuarial model would predict, “Your ultimate redemption rate is 80% today, and will grow to 85% by year end”” reflecting real-world variations in redemption behavior.This insight enables CFOs to make accurate financial plans so there is no surprise at year end when the URR comes in at 85% but the plan was expecting 80%. These variances from plan can drive significant financial volatility because the size of the liability is often extremely large, so even small changes in the URR can drive multi-million-dollar impacts.

4. Limited Transparency vs. Audit-Ready Reporting

Financial models often lack detailed transparency, making it harder for CFOs and finance teams to justify liability estimates to auditors.

Actuarial models provide detailed, data-driven reports that align with accounting and auditing standards, making it easier to defend liability estimates during audits.

What’s the impact? A financial model may assume a 75% redemption rate without providing supporting evidence, leaving finance teams vulnerable to auditor scrutiny.An actuarial model, however, backs its URR estimate with granular, data-driven insights, such as customer segmentation and historical redemption trends.This statistical rigor not only strengthens financial reporting but also streamlines audits by providing clear, defensible liability estimates.

When Is a Financial Model Enough?

Not every loyalty program needs an actuarial model. For smaller programs, early-stage launches, or short-horizon planning, a well-built financial model may be entirely appropriate. Specifically, financial modeling is likely sufficient when:

- The program is small — liability is immaterial relative to the balance sheet and auditor scrutiny is low

- The planning horizon is short — you’re modeling the next quarter, not multi-year accruals

- The use case is strategic, not accounting — building a business case for a new benefit tier, not filing a 10-K footnote

- No external audit requirement exists — private companies with no reporting obligations have more latitude

The threshold changes when the liability becomes material, when auditors start asking questions, or when the program is connected to a significant financial event (IPO, acquisition, debt covenant). That’s when the distinction between a financial assumption and a statistically defensible estimate stops being academic.

When Does a Loyalty Program Need an Actuary?

Several trigger events make actuarial modeling the right — and sometimes required — choice:

- Audit committee questions. When auditors start asking how you derived your breakage or URR assumptions, a financial model’s answer (“we used an industry benchmark”) isn’t sufficient. An actuarial model provides a credentialed opinion.

- Material liability. As programs scale, points liability can represent tens or hundreds of millions on the balance sheet. At that scale, the cost of being wrong dwarfs the cost of getting it right.

- IPO or acquisition. Buyers, underwriters, and SEC reviewers will scrutinize loyalty liability estimates. Actuarial backing is increasingly expected.

- New program launch. Building the liability framework correctly from the start avoids expensive retrofits when the program grows and auditors arrive.

- Program changes. New earn/burn structures, partner integrations, or expiration policy changes materially affect redemption behavior — and your existing model may not capture the shift.

If any of these apply, the question isn’t whether to bring in actuarial expertise — it’s how quickly.

How KYROS Solves These Problems

KYROS eliminates the risks of assumption-based financial modeling by providing actuarial expertise tailored specifically for loyalty programs.

Data-Driven, Predictive Modeling

Unlike financial models that rely on static assumptions, KYROS uses statistical and predictive models to estimate liability based on real-world redemption behavior. This ensures finance teams always have accurate, dynamic forecasts instead of outdated estimates.

Audit-Ready, Transparent Reporting

Financial modeling often leads to auditor scrutiny due to a lack of supporting data. KYROS provides detailed, defensible Actuarial Opinion reports that align with accounting, auditing, and actuarial professional standards, making audits smoother and compliance easier.

Smarter Decision-Making with Predictive Insights

KYROS’ models don’t just estimate liability—they forecast future trends, allowing companies to:

- Adjust financial reserves proactively.

- Improve budgeting accuracy.

- Support strategic decisions with real-time data.

Loyalty-Specific Expertise

KYROS is the only actuarial firm focused exclusively on loyalty programs, providing the specialized insights finance teams need to ensure liability is accurately managed and optimized for long-term stability.

The Right Model for the Right Job

Financial modeling plays a role in loyalty programs, but when it comes to liability estimation, actuarial modeling is essential for accuracy, compliance, and strategic decision-making.

For finance teams looking to eliminate uncertainty and optimize liability management, KYROS provides the expertise, data-driven modeling, and transparent reporting needed to ensure financial stability.

If your company is still relying on financial modeling for liability estimation, now is the time to rethink your approach.