Imagine a CFO presenting loyalty program liability estimates to their auditors, confident in the numbers.

The team used a financial model based on industry-standard assumptions. But when the audit begins, the red flags go up—the estimates don’t align with actual redemption patterns, liability fluctuations raise concerns, and the auditors push back.

The company is now facing a major compliance risk, all because their financial model wasn’t built for this purpose.

This scenario happens more often than you’d think.

Many finance leaders assume that financial modeling and actuarial modeling are interchangeable when it comes to loyalty program liability. In reality, they serve completely different functions.

Using financial modeling alone for liability estimation is like using a ruler to measure a storm—it’s the wrong tool for the job.

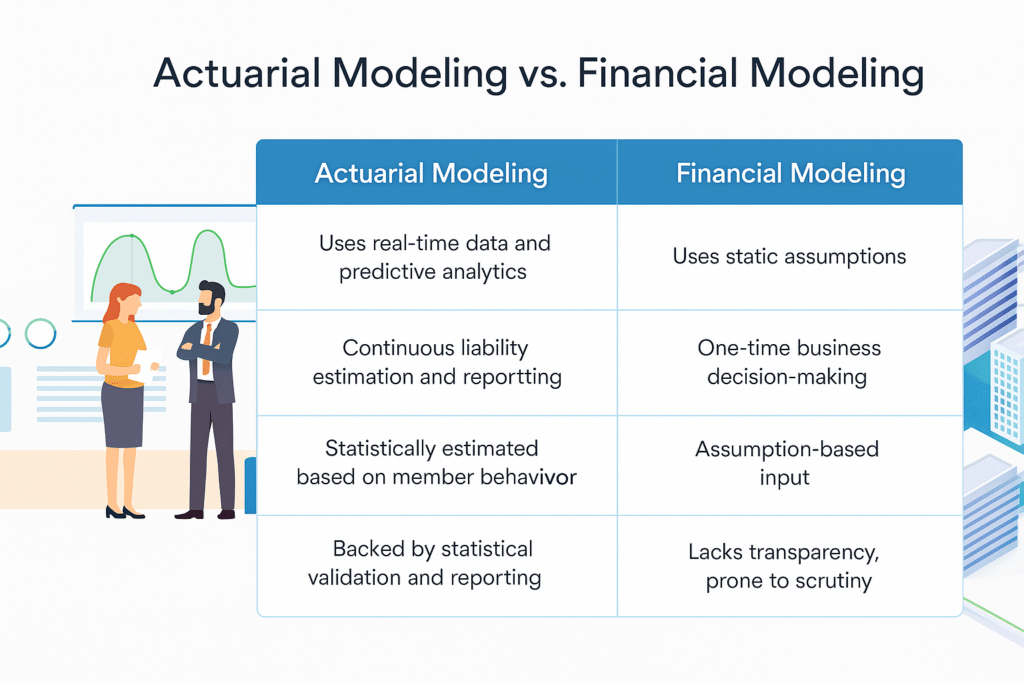

Financial models rely on static assumptions, while actuarial models extract real-world insights from massive data sets to produce precise, dynamic forecasts. This distinction isn’t just theoretical—it has direct financial implications. A miscalculated liability can lead to financial misstatements, balance sheet volatility, and costly audit challenges.

In this article, we’ll break down the differences between financial modeling and actuarial modeling, show why it matters for CFOs, and explain how an actuarial approach provides the accuracy and stability needed to avoid financial pitfalls.

The Key Differences Between Financial Modeling and Actuarial Modeling

Many finance leaders assume that if they have a financial model for their loyalty program, they also have a reliable liability estimate.

In reality, financial models and actuarial models serve very different purposes—and using the wrong one for liability estimation can have serious consequences.

Let’s break down the key differences between the two.

1. Assumptions vs. Data-Driven Insights

Financial models rely on high-level assumptions. They use industry benchmarks or fixed inputs, such as an assumed Ultimate Redemption Rate (URR), to estimate liability.

Actuarial models, on the other hand, are built using massive volumes of real data. Rather than assuming a redemption rate, actuarial models extract behavioral patterns from loyalty program members to directly estimate URR with statistical accuracy.

What’s the impact? A financial model might assume a 75% redemption rate, but where did this estimate come from and how is it justified?The financial model didn’t produce this estimate; it was plugged in as an assumption. An actuarial model, on the other hand, analyzes customer data at a granular level to directly estimate the URR using robust statistical and actuarial methods so the accuracy can be easily justified and documented.The actuarial model may find that the 75% assumption to be wrong, and the true URR is 90%. In this case, you’d be running your loyalty business model with a materially wrong understanding of your cost structure.Redemption cost is often the single largest expense in the business model, so this is a significant issue. If you didn’t have an actuarial model in place, you would be digging a huge financial hole in your business and wouldn’t even know it.

2. One-Time Use vs. Continuous Monitoring

Financial models are typically used once—for example, when building a business case for launching or adjusting a loyalty program.

Actuarial models are designed for continuous, real-time monitoring of liability. Since redemption behavior shifts over time, actuarial models dynamically update, ensuring ongoing accuracy in liability estimation.

What’s the impact? A financial model from five years ago may assume a redemption rate that no longer reflects current customer behavior.An actuarial model, however, continuously updates based on real-time data, accounting for recent trends such as increased engagement from a new partnership or reduced redemptions due to economic downturns.Without these updates, finance teams risk misallocating reserves, either tying up unnecessary capital or underfunding liabilities, leading to financial instability.

3. Static Estimates vs. Predictive Forecasting

Financial models generate a static estimate at a given point in time. They provide a snapshot but don’t predict how liability will shift over time.

Actuarial models leverage predictive analytics to forecast liability trends, giving finance leaders a forward-looking view that allows them to adjust business strategies proactively.

What’s the impact? A financial model might state, “Your ultimate redemption rate is 80%,” treating it as a fixed number that doesn’t change over the course of the year. However, an actuarial model would predict, “Your ultimate redemption rate is 80% today, and will grow to 85% by year end”” reflecting real-world variations in redemption behavior.This insight enables CFOs to make accurate financial plans so there is no surprise at year end when the URR comes in at 85% but the plan was expecting 80%. These variances from plan can drive significant financial volatility because the size of the liability is often extremely large, so even small changes in the URR can drive multi-million-dollar impacts.

4. Limited Transparency vs. Audit-Ready Reporting

Financial models often lack detailed transparency, making it harder for CFOs and finance teams to justify liability estimates to auditors.

Actuarial models provide detailed, data-driven reports that align with accounting and auditing standards, making it easier to defend liability estimates during audits.

What’s the impact? A financial model may assume a 75% redemption rate without providing supporting evidence, leaving finance teams vulnerable to auditor scrutiny.An actuarial model, however, backs its URR estimate with granular, data-driven insights, such as customer segmentation and historical redemption trends.This statistical rigor not only strengthens financial reporting but also streamlines audits by providing clear, defensible liability estimates.

How KYROS Solves These Problems

KYROS eliminates the risks of assumption-based financial modeling by providing actuarial expertise tailored specifically for loyalty programs.

Data-Driven, Predictive Modeling

Unlike financial models that rely on static assumptions, KYROS uses statistical and predictive models to estimate liability based on real-world redemption behavior. This ensures finance teams always have accurate, dynamic forecasts instead of outdated estimates.

Audit-Ready, Transparent Reporting

Financial modeling often leads to auditor scrutiny due to a lack of supporting data. KYROS provides detailed, defensible Actuarial Opinion reports that align with accounting, auditing, and actuarial professional standards, making audits smoother and compliance easier.

Smarter Decision-Making with Predictive Insights

KYROS’ models don’t just estimate liability—they forecast future trends, allowing companies to:

-

Adjust financial reserves proactively.

-

Improve budgeting accuracy.

-

Support strategic decisions with real-time data.

Loyalty-Specific Expertise

KYROS is the only actuarial firm focused exclusively on loyalty programs, providing the specialized insights finance teams need to ensure liability is accurately managed and optimized for long-term stability.

The Right Model for the Right Job

Financial modeling plays a role in loyalty programs, but when it comes to liability estimation, actuarial modeling is essential for accuracy, compliance, and strategic decision-making.

For finance teams looking to eliminate uncertainty and optimize liability management, KYROS provides the expertise, data-driven modeling, and transparent reporting needed to ensure financial stability.

If your company is still relying on financial modeling for liability estimation, now is the time to rethink your approach.