If you issue points every month and your redemption-cost assumptions are off, the error accumulates. You often don’t notice until redemptions begin arriving faster (or at higher ultimate rates) than expected and then you’re explaining a budget hole that can dwarf the “error” you made in any single month.

Forecasting redemption costs is less about perfect prediction and more about risk management:

- Protect the ROI denominator from wishful thinking.

- Give finance a credible forecast to plan against.

- Plan promotions without accidentally creating an unfunded redemption wave.

What you’re forecasting

At minimum, you’re forecasting:

- Ultimate Redemption Rate (URR): of what you issue, what share will ultimately be redeemed

- Timing: when will redemptions arrive (next month vs next year)?

- Cost: what will those redemptions cost the business?

The key reality: URR changes over time as your earning member mix and behaviors change. If you’re doing a good job, you may accumulate more engaged members who are more likely to redeem, so URR can rise (often a good sign), but your model must reflect it otherwise you’re running your business with the wrong assumptions for the single largest expense in the loyalty business model.

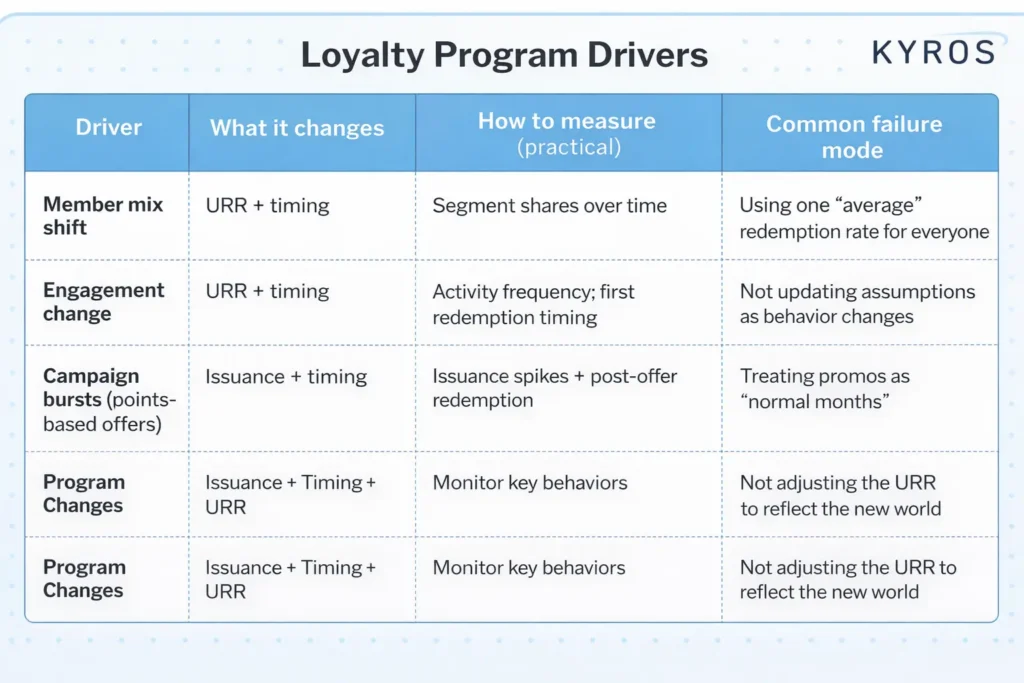

The drive table – what moves your forecast

Two Mini Examples

Example 1 – Accumulating Error

You issue 1B points/month and assume 70% will redeem at $0.01/point:

- Forecasted ultimate cost per month of issuance: 1B × 70% × $0.01 = $7,000,000

- True cost per month of issuance: 1B × 80% × $0.01 = $8,000,000

If your true URR is 80% (due to mix/behavior change) but your models don’t pick it up:

That’s a $1,000,000/month gap. This may not be a big deal relative to the entire business. But if it goes unnoticed for 24 months, you’ve created a $24,000,000 financial hole—before timing effects and promotions. If it continues even longer without notice, the financial hole accumulates to something even larger.

Example 2 – Mix shift moves URR even when issuance is flat

If the share of issued points shifts toward more engaged earners, your blended URR rises even when issuance doesn’t. The takeaway: watch who is earning (mix) as much as how much you’re issuing.

How to start without gaming ROI

If you don’t have a clean loyalty P&L, a finance-safe first step is:

- Start with redemption cost in the denominator.

- State clearly: “This is ROI vs variable reward cost (gross margin context).”

- Expand in stages as you mature cost tagging and governance.

Consistency beats completeness early. Finance will trust a stable definition more than a shifting “full cost” claim.

Ignoring redemption assumptions can create fake ROI

If you assume issued points will cost $1.0M to redeem but true redemption cost is $1.4M (because behavior changed), your ROI can flip sign months later. This isn’t just an accounting nuance—errors accumulate over time.